Freedom Portfolios: Managing for Inflation Expectations

- Gordon McMahan

- May 17, 2021

- 5 min read

The diversified mix of investments in Freedom portfolios seeks to mitigate the risk associated with rising prices as inflation normalizes.

Inflation is an increase in the cost of goods and services – and it’s a hot topic causing some concern among investors. Because any form of uncertainty regarding your finances can be stressful, let’s take a few minutes to discuss what’s happening, put it into perspective and understand how the Asset Management Services (AMS) Investment Committee (IC) manages Freedom portfolios with an eye toward inflation.

Inflation is typically caused by two factors. When the cost to produce something rises, companies will pass the increased expense along to the consumer by raising prices – this is called cost-push inflation. Companies can also raise prices when demand for something is high and people are willing to pay more to get it – this is called demand-pull inflation.

For much of the past decade, as the economy recovered from the Great Recession, inflation was consistently around or below the U.S. Federal Reserve’s 2.0% target, the amount of inflation it considers healthy for a steadily growing economy.

Now, as the economy continues to recover from the slowdown of the COVID-19 pandemic, inflation uncertainty is reaching a high point. There is concern for he effects of unprecedented fiscal stimulus, low interest rates, increased government debt, a tightening labor market, supply chain bottlenecks and more. Both inflation scenarios appear to be in play.

Companies are indicating they may need to raise their prices to offset the increasing cost of commodities used to produce their goods and services. Also, people may feel they have more money to spend, given the influx of cash from trillion-dollar stimulus efforts, and be willing to pay more for what they want. Demand- pull inflation could even be a self-fulfilling prophecy in which people buy now for fear prices will increase in the future, creating the very demand that drives prices higher.

Some theorize a long-term inflation shock could occur, reaching levels of 3.0% to 3.5% over a longer time period, and that sustained inflation above the Federal Reserve’s 2.0% target could compel it to raise interest rates sooner than planned, stunting economic growth. That, however, is not the expectation of the AMS IC, which has taken steps to prepare Freedom portfolios for what it views to be inflation normalization.

The AMS IC View: Normalization

The AMS IC, the team of experienced professionals that oversees the Freedom investment process, believes inflation will be higher than in recent years, but does not expect it to be abnormally high for an extended period:

Inflation will be transitory – after dropping sharply in 2020, it will rise in 2021 before settling into a normalized range of 2.0% to 2.5%.

Inflation of 2.2% for the next several years has been factored into the management of Freedom portfolios, including the overall mix of equity and fixed income.

A Basket of Goods

The most common measurement for inflation is the Consumer Price Index (CPI). The CPI is a basket of goods and services from several categories such as apparel, food, transportation, housing and medical care. Prices are gathered, weighted and averaged to determine whether the same basket of goods costs consumers more or less over time.

The chart below tracks inflation over the past two decades by two measurements: CPI is the full basket of goods and services, while Core CPI removes the more volatile goods from the basket, such as food and gasoline, to provide a more stable view of inflation. Core data is used to inform the Federal Reserve’s monetary policy.

The chart shows Core CPI dipped noticeably three times in the past two decades: 2003, 2010 and 2020. In 2003 and 2010, the dips were followed by periods of Core CPI inflation slightly above the Federal Reserve’s 2.0% target, even as the full CPI climbed much higher.

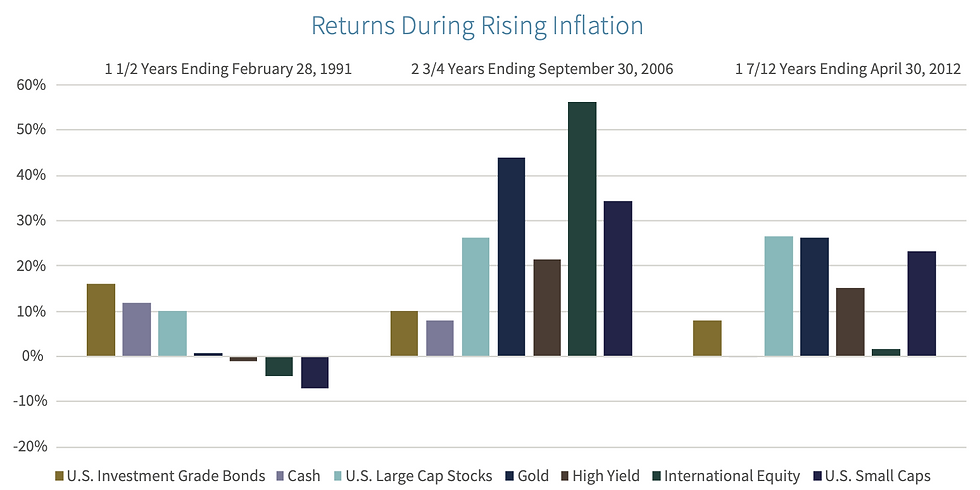

Investing During Inflationary Periods

The chart below shows cumulative returns for five major asset classes, plus gold and cash, during the inflationary periods of 1990-91, 2004-06 and 2010-12. Though performance varied within the type of equity – international equity led the way from 2004-06, but lagged during the other periods – equity and high yield bonds consistently outperformed high quality bonds. Gold and cash were relatively inconsistent performers across all three inflationary periods.

Freedom Positioning

Equities have historically performed well during inflationary periods. The AMS IC recently moved Freedom portfolios to an overweight position in equity exposure. Believing the U.S. economy is better-positioned than others to recover more quickly, the overweight is expressed in U.S. equities across capitalizations.

Given the Fed’s reliance on Core CPI to assess inflation, and its pledge to keep rates at current levels until 2023, interest rates are expected to remain low. The AMS IC recently moved Freedom portfolios to an underweight position in fixed income , achieved by underweighting high-quality fixed income relative to normal targets. There is also a slight overweight to high yield bonds, which act more like equities.

Conclusion

Even as heightened uncertainty regarding inflation makes headlines, the IC believes inflation will normalize – a rise in 2021 will occur before settling into a normal range of 2.0% to 2.5% for the long term. This expectation is accounted for in Freedom portfolio positioning.

The AMS IC evaluates Freedom portfolios on a continuous basis. It will continue to monitor the inflation outlook and make data- dependent decisions, as necessary. Any changes would be in an attempt to earn the best possible return for the amount of downside risk the committee is willing to tolerate, in alignment with portfolio objectives.

To read the entire white paper, please click here.

Have questions or need financial guidance? We're always here to help. Please contact us.

The foregoing content reflects the opinions of Raymond James Asset Management Services and is subject to change at any time without notice. Content provided herein is for informational purposes only and should not be construed as investment advice or a recommendation regarding the purchase or sale of any security outside of a managed account. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. All investments are subject to risk and you may incur a profit or a loss. There is no assurance that any investment strategy will be successful. Asset allocation and diversification does not ensure a profit or protect against a loss. Past performance is not a guarantee of future results.

In a fee-based account, clients pay a quarterly fee, based on the level of assets in the account, for the services of a financial advisor as part of an advisory relationship. In deciding to pay a fee rather than commissions, clients should understand that the fee may be higher than a commission alternative during periods of lower trading. Advisory fees are in addition to the internal expenses charged by mutual funds and other investment company securities. To the extent that clients intend to hold these securities, the internal expenses should be included when evaluating the costs of a fee-based account. Clients should periodically re-evaluate whether the use of an asset-based fee continues to be appropriate in servicing their needs. These additional considerations, as well as the Freedom fee schedule, are listed more fully in the Client Agreement and the Raymond James & Associates Wrap Fee Brochure.

Comments